One of the most important decisions with any savings plan, particularly KiwiSaver and other superannuation schemes, is asset allocation. Asset allocation is the outcome of a process that aims to balance the risk and rewards of a portfolio after considering an individual’s goals, risk tolerance and investment horizon.

There are two main asset classes in the asset allocation process; high risk growth assets, mainly shares, and low risk income assets, comprising bonds and cash. The asset allocation decision has a huge impact on the risk profile and performance of a portfolio.

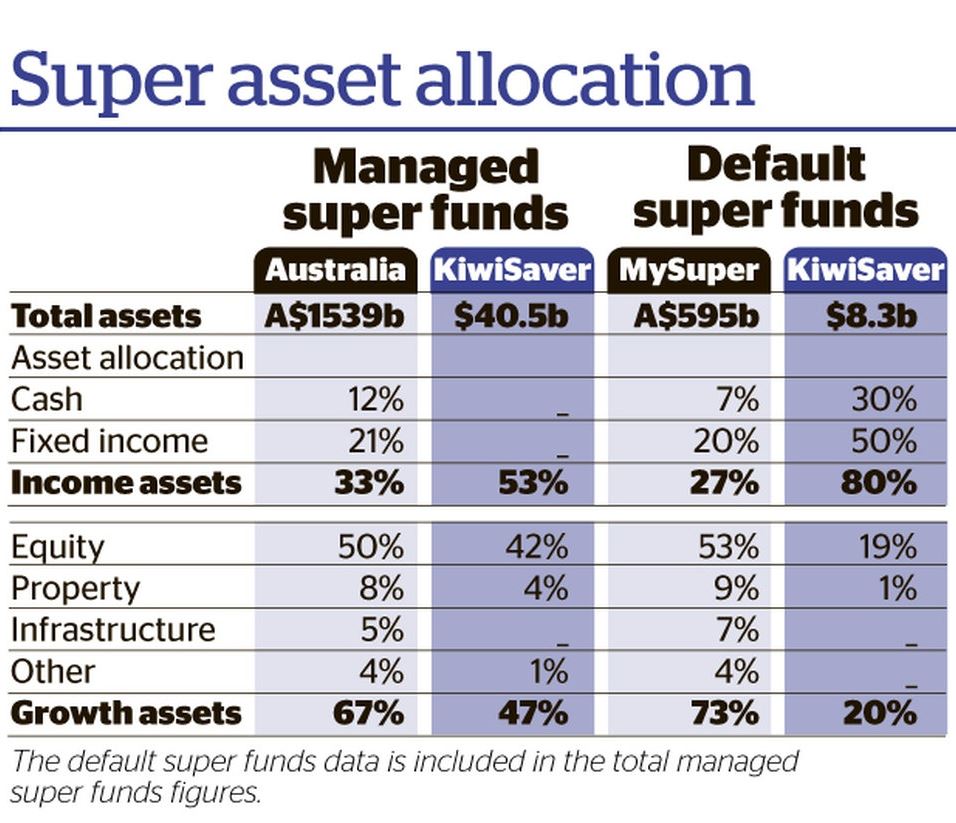

There are two distinct superannuation vehicles in New Zealand and Australia.

New Zealanders have KiwiSaver and other registered superannuation, mainly the old company superannuant schemes. These schemes have $66.7 billion under management with KiwiSaver comprising $40.5b according to Morningstar, and other registered superannuation $26.2b.

KiwiSaver is growing rapidly and replacing the more traditional superannuation schemes.

Australians have managed superannuation funds and self-managed super funds (SMSF), both of which are compulsory. The two schemes have A$2,236b ($2,428b) under management with managed superannuation funds having total assets of A$1,539b according to the Australian Prudential Regulation Authority (APRA) and SMSFs A$697b.

The following statistics clearly demonstrate that New Zealanders are underfunded for retirement, particularly compared with their transtasman neighbours.

- Australian have superannuation savings of A$91,000 per capita compared with only $14,000 per capita on this side of the Tasman.

- Total superannuation funds represent 130 per cent of Australia’s GDP whereas our superannuation savings represent only 26 per cent of the country’s GDP.

- New Zealanders own houses and land worth $771b compared with superannuation funds of only $66.7b while Australians have houses and land worth A$6,271b compared with super funds of A$2,236b. Thus, the residential property to superannuation ratio is only 2.8 times in Australia compared with 11.6 times in New Zealand.

New Zealanders are asset rich in terms of property holdings but, at this stage, have relatively less liquid funds available for their retirement.

KiwiSaver and Australian superannuation managed funds (excluding SMSFs) achieved identical net returns of 9.2 per cent per annum in the five years to June 2017. However, there was a significant difference between the performance of high risk and low risk funds as outlined in Morningstar’s June Quarter 2017 KiwiSaver Survey:

- Conservative KiwiSaver funds, which had an average allocation of only 19 per cent to growth assets, reported average returns of only 6.4 per cent for the five years to June 2017.

- Moderate funds, with a 34 per cent allocation to growth assets, had an average return of 7.3 per cent.

- Balanced funds, with a 54 per cent allocation to growth assets, reported average returns of 9.8 per cent.

- Growth funds, with 74 per cent invested in growth assets, achieved a 12.1 per cent annualised return.

Aggressive funds, with 86 per cent in growth assets, achieved a return of 12.4 per cent per annum for the five-year period.

KiwiSaver funds have had a great opportunity to outperform Australian superannuation funds since June 2012 because the NZX benchmark index surged 124 per cent over this five-year period while the ASX benchmark increased by a more modest 75 per cent. However, our conservative approach towards asset allocation has had a negative impact on total KiwiSaver returns.

One of the biggest differences between Australia and New Zealand superannuation are the default funds with A$595b and $8.3b under management respectively.

Australian default superannuation funds, called MySuper, provide a low-cost alternative to employers and employees. MySuper options have several basic features, including low fees. They also allow members to compare funds easily based on cost, investment performance and insurance.

According to the Australian Securities & Investment Commission (ASIC), it is common for these default MySuper funds to have a balanced/growth approach to investing with a 70 per cent allocation to growth assets (e.g. shares and property) and 30 per cent to defensive investments (e.g. cash and fixed interest).

This asset allocation policy is clearly illustrated in the accompanying table with MySuper default funds having 73 per cent invested in higher risk growth assets at the end of June 2017 and only 27 per cent in defensive income assets.

By comparison, KiwiSaver default schemes are designed to give stable returns. They have a conservative approach, with a 15 per cent to 25 per cent allocation to growth assets.

The stable returns approach to default KiwiSaver funds is in total contrast to the more aggressive approach adopted by Australia’s MySuper default funds. For example:

- KiwiSaver default funds have 30 per cent invested in cash compared with only 7 per cent allocated to cash by MySuper.

- KiwiSaver default products have 50 per cent of total assets invested in fixed interest securities compared with only 20 per cent by MySuper.

- KiwiSaver default funds have only 20 per cent invested in growth assets compared with 73 per cent allocated to growth assets through MySuper.

The asset allocation, and performance, of these default funds has a major impact on KiwiSaver’s total asset allocation. The major differences between KiwiSaver and Australian managed super funds are:

- KiwiSaver has only 47 per cent of total assets allocated to growth assets compared with 67 per cent for Australian managed super funds.

- KiwiSaver has a high allocation to cash and fixed interest securities with lower risk income assets representing 53 per cent of total assets compared with 33 per cent for Australian super.There is a strong argument that superannuation asset allocation is heavily influenced by one important factor, whether schemes are compulsory or voluntary.

KiwiSaver, which is voluntary, has a conservative asset allocation because there are concerns that members will stop contributing if they experience negative returns.

By contrast, under Australia’s compulsory structure individuals must continue to contribute, regardless of the performance of their portfolio. Thus, compulsory schemes can have a much higher risk profile than voluntary superannuation schemes because members must continue to contribute, regardless of the historic performance of their funds. KiwiSaver has been a huge success and there is a strong argument that changes shouldn’t be made to a scheme that has clearly exceeded initial expectations.

However, a decade after inception, a tweak or two is warranted, particularly in relation to default funds. These changes could include:

- KiwiSaver default funds should have a strong aggressive/growth asset allocation bias for all members under 35 years of age.

- Default funds could have a balanced bias for members between 35 and 50 years of age.

- Default funds could have a moderate/conservative bias for member over 50 years of age.

These changes would raise the risk profile, and long-term returns, of default KiwiSaver members who begin contributing at an early age but would largely maintain the current low risk profile of those over 50.

Brian Gaynor

is an investment analyst and the Executive Director of Milford Asset

Management.

No comments:

Post a Comment